13 Sep Best Value Case Study – Recycling Services

A large organization was introduced to the Best Value Approach (BVA) in 2017. After reviewing the documentation and results of BVA, the client was interested in running a test-project using the BVA. The organization was recommended to identify a project that would be suited in showing the versatility, and high performance of the BVA. The first test project was identified as the recycling services for the facilities in a specific area.

The organization considered the project to be high risk because of their limited amount of information, and broad scope of work. After discussing the risks of the project, the client team made the decision to use a BVA consultant to guide them through their first pilot project using the BVA.

Preparation Phase

The client was looking to procure recycling services from a vendor that could meet the requirements of the local ordinance as well as produce the most value for the organization in terms of revenue, environmental impact, and legal requirements.

The requirement of this project included:

- Meet the requirements of the local ordinance for recycling programs for one year with options to renew.

- Output “from the curb” of waste and recyclable materials.

- Minimize the amount of material sent to the landfill.

- Maximize the revenue of recyclable materials to the client.

- Meet the current legal and operational requirements of the client.

The RFP was advertised to recycling and waste vendors in the state. Two recycling vendors and two waste haulers attended the education session.

Selection Phase

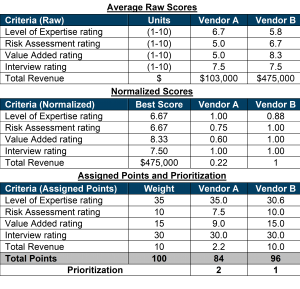

The organization received two proposals from recycling vendors, which we will call Vendor A and Vendor B. Each written submittal was evaluated, and the ratings identified a clear difference in the quality of the vendors’ proposals. The selection committee interviewed both vendors. The interview ratings were added to the submittal ratings.

The ratings for the submittals and proposed revenue were put into the selection matrix including their raw scoring and revenue, normalized scores, and awarded points and prioritization (Table 1). Vendor B was identified as the best value vendor.

The performance information was shown to the entire selection committee. They unanimously supported Vendor B as the best value vendor.

The performance information was shown to the entire selection committee. They unanimously supported Vendor B as the best value vendor.

Clarification Phase

Vendor B worked on creating a plan that would address all the concerns and worries of the client. It was important that the plan was simple enough for all stakeholders to understand. Vendor B presented their plan to the stakeholders. All stakeholders approved the plan and meetings were set up with the individual stakeholders to discuss the implementation plan in their specific areas. The vendor’s plan was identified as very competitive because of the following reasons:

- The plan provided services beyond the RFP requirements. It not only included the management of recycling services, but also took over the billing of all waste and recycling services which relieved that responsibility from the client’s stakeholder.

- The vendor’s WRR included the vendor’s commitment to provide total transparency reporting on the recycling revenue, waste expenses, and Vendor B’s charges.

- The plan proposed that the vendor would track and suggest changes to increase revenue and minimize waste.

- The vendor came up with an innovative pricing model that would not charge a management fee for recycling and waste management but would take 22% of all recycling revenue and give the client 78%. This would allow pricing to be fair regardless of changes in recycling material prices or changes in the recycling industry.

- The plan would accommodate all implementation costs.

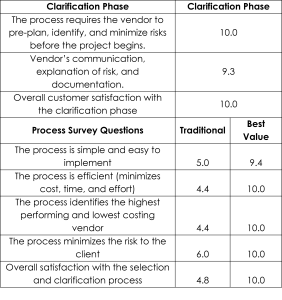

The seven stakeholders working on the project were given surveys to rate the BVA process compared to the traditional process. The results are presented in Table 2. The results of the procurement process were also compiled to show the performance of the method in Table 3.

Execution Phase

Vendor B was committed to creating transparency and simplifying the recycling revenues and waste services costs. As soon as Vendor B started the execution portion of the project, there were major changes in the recycling market that greatly affected the vendor’s revenue projections. Vendor B created a WRR that explained all the deviations and created transparency for the organization.

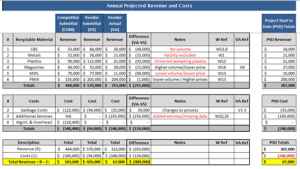

Table 4 is the year 1 WRR which documented the following:

- The expert vendor submitted revenue.

- Changes made to the revenue in changed conditions [risk outside of the vendor’s control].

- Changes made to costs [outside the vendor’s control].

- The original baseline revenue and cost of the previous year.

The information tracked in the WRR allowed the stakeholders to immediately see the impact of risk, and that the client is far better off with the expert vendor rather than the competitor.

Conclusion

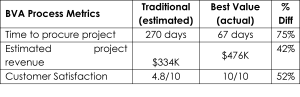

The testing of the BVA to deliver recycling services was a success [75% faster, 42% increased revenue, 52% increased customer satisfaction, minimized bureaucracy and management, direction and control].

The Weekly Risk Report (WRR) gave the client an accurate view of the services being provided. The WRR minimized the client stakeholders’ decision making. Using the information, the client stakeholders changed their structure and personnel to facilitate the expert’s recommendations.

The expert vendor’s contract was renewed for year two. The expert’s expertise is now being used by the client stakeholder to change their in-house operations to minimize their cost. The expert vendor is now treated as a part of the client’s stakeholder system.